CLARKESVILLE, Ga. — Final September, Alton Fry went to the physician involved he had hypertension. The journey would end in a prostate most cancers analysis.

So started the stress of attempting to pay for tens of hundreds of {dollars} in remedy — with out medical insurance.

“I’ve by no means been sick in my life, so I’ve by no means wanted insurance coverage earlier than,” mentioned Fry, a 54-year-old self-employed masonry contractor who restores outdated buildings within the rural Appalachian neighborhood he’s known as dwelling practically all his life.

Ensuring he had insurance coverage was the very last thing on his thoughts, till just lately, Fry mentioned. He had been rebuilding his life after a jail keep, sustaining his sobriety, restarting his enterprise, and remarrying his spouse. “Issues acquired busy,” he mentioned.

Now, with a family earnings of about $48,000, Fry and his spouse earn an excessive amount of to qualify for Georgia’s restricted Medicaid enlargement. And he mentioned he discovered that the well being plans bought on the state’s Reasonably priced Care Act trade have been too costly or the protection too restricted.

In late April, a good friend launched a crowdfunding marketing campaign to assist Fry cowl a number of the prices. To save cash, Fry mentioned, he’s taking a much less aggressive remedy route than his physician beneficial.

“There isn’t any assist for middle-class America,” he mentioned.

Greater than 26 million Individuals lacked medical insurance within the first six months of 2024, in keeping with the Facilities for Illness Management and Prevention.

The uninsured are largely low-income adults underneath age 65, and folks of shade, and most stay within the South and West. The uninsured charge within the 10 states that, like Georgia, haven’t expanded Medicaid to just about all low-income adults was 14.1% in 2023, in contrast with 7.6% in enlargement states, in keeping with KFF, a well being info nonprofit that features KFF Well being Information.

Well being coverage researchers anticipate the variety of uninsured to swell because the second Trump administration and a GOP-controlled Congress attempt to enact insurance policies that explicitly roll again well being protection for the primary time for the reason that creation of the trendy U.S. well being system within the early twentieth century.

Below the “One Massive Stunning Invoice Act” — finances laws that may obtain a few of President Donald Trump’s priorities, like extending tax cuts primarily benefiting the rich — some 10.9 million Individuals would lose medical insurance by 2034, in keeping with estimates by the nonpartisan Congressional Finances Workplace based mostly on a Home model of the finances invoice.

A Senate model of the invoice may end in extra folks dropping Medicaid protection, with reductions in federal spending and guidelines that may make it more durable for folks to qualify. However that invoice suffered a serious blow June 26 when the Senate parliamentarian, a nonpartisan official who enforces the chamber’s guidelines, rejected a number of well being provisions — together with the proposal to steadily scale back supplier taxes, a mechanism that almost each state makes use of to extend its federal Medicaid funding.

The quantity may rise to 16 million if proposed rule modifications to the ACA take impact and tax credit that assist folks pay for ACA plans expire on the finish of the 12 months, in keeping with the CBO. In KFF ballot outcomes launched in June, practically two-thirds of individuals surveyed seen the invoice unfavorably and greater than half mentioned they have been apprehensive federal funding cuts would harm their household’s skill to acquire and afford well being care.

Like Fry, extra folks could be pressured to pay for well being bills out-of-pocket, resulting in delays in care, misplaced entry to wanted medical doctors and drugs, and poorer bodily and monetary well being.

“The consequences might be catastrophic,” mentioned Jennifer Tolbert, deputy director of KFF’s Program on Medicaid and the Uninsured.

The Home-passed invoice would symbolize the biggest discount in federal help for Medicaid and well being protection in historical past, she mentioned. If the Senate approves it, it might be the primary time Congress moved to eradicate protection for tens of millions of individuals.

“This may take us again,” Tolbert mentioned.

A Patchwork System

America is the one rich nation the place a considerable variety of residents lack medical insurance, because of practically a century of pushback towards common protection from medical doctors, insurance coverage corporations, and elected officers.

“The complexity is all over the place all through the system,” mentioned Sherry Glied, dean of New York College’s Wagner College of Public Service, who labored within the George H.W. Bush, Clinton, and Obama administrations. “The large bug is that individuals fall between the cracks.”

This 12 months, KFF Well being Information is chatting with Individuals concerning the challenges they face find medical insurance and the results on their skill to get care; to suppliers who serve the uninsured; and to coverage consultants about why, even when the nation hit its lowest recorded uninsured charge in 2023, practically a tenth of the U.S. inhabitants nonetheless lacked well being protection.

To date, the reporting has discovered that regardless of many years of insurance policies designed to extend entry to care, the very construction of the nation’s medical insurance system creates the other impact.

Authorities-backed common protection has eluded U.S. policymakers for many years.

After lobbying from doctor teams, President Franklin D. Roosevelt deserted plans to incorporate common well being protection within the Social Safety Act of 1935. Then, due to a wage and wage cap used to regulate inflation throughout World Battle II, extra employers supplied medical insurance to lure staff. In 1954, well being protection was formally exempted from earnings tax necessities, which led extra employers to supply the profit as a part of compensation packages.

Insurance coverage protection supplied by employers got here to type the muse of the U.S. well being system. However ultimately, issues with linking medical insurance to employment emerged.

“We realized, effectively, wait, not all people is working,” mentioned Heidi Allen, an affiliate professor on the Columbia College of Social Work who research the impression of social insurance policies on entry to care. “Youngsters aren’t working. People who find themselves aged should not working. Individuals with disabilities should not working.”

But subsequent efforts to broaden protection to all Individuals have been met with backlash from unions who needed medical insurance as a bargaining chip, suppliers who didn’t need authorities oversight, and those that had protection via their employers.

That led policymakers so as to add applications piecemeal to make medical insurance accessible to extra Individuals.

There’s Medicare for older adults and Medicaid for folks with low incomes and disabilities, each created in 1965; the Youngsters’s Well being Insurance coverage Program, created in 1997; the ACA’s trade plans and Medicaid enlargement for individuals who can’t entry job-based protection, created in 2010.

In consequence, the U.S. has a patchwork of medical insurance applications with quite a few curiosity teams vying for {dollars}, somewhat than a cohesive system, well being coverage researchers say.

Falling By means of the Cracks

The dearth of a cohesive system signifies that, regardless that Individuals are eligible for medical insurance, they wrestle to entry it, mentioned Mark Shepard, an affiliate professor of public coverage on the Harvard Kennedy College of Authorities. No central entity exists within the U.S. to make sure that all folks have a plan, he mentioned.

Over half of the uninsured would possibly qualify for Medicaid or subsidies that may assist cowl the prices of an ACA plan, in keeping with KFF. However many individuals aren’t conscious of their choices or can’t navigate overlapping applications — and even backed protection might be unaffordable.

Those that have fallen via the cracks mentioned it feels just like the system has failed them.

Yorjeny Almonte of Allentown, Pennsylvania, earns about $2,600 a month as an inspector in a cupboard warehouse. When she began her job in December 2023, she didn’t wish to spend practically 10% of her earnings on medical insurance.

However, final 12 months, her uninsured mother selected to fly to the Dominican Republic to get look after a well being concern. So Almonte, 23, who additionally wanted to see a physician, investigated her employer’s well being choices. By then she had missed the deadline to enroll.

“Now I’ve to attend one other 12 months,” she mentioned.

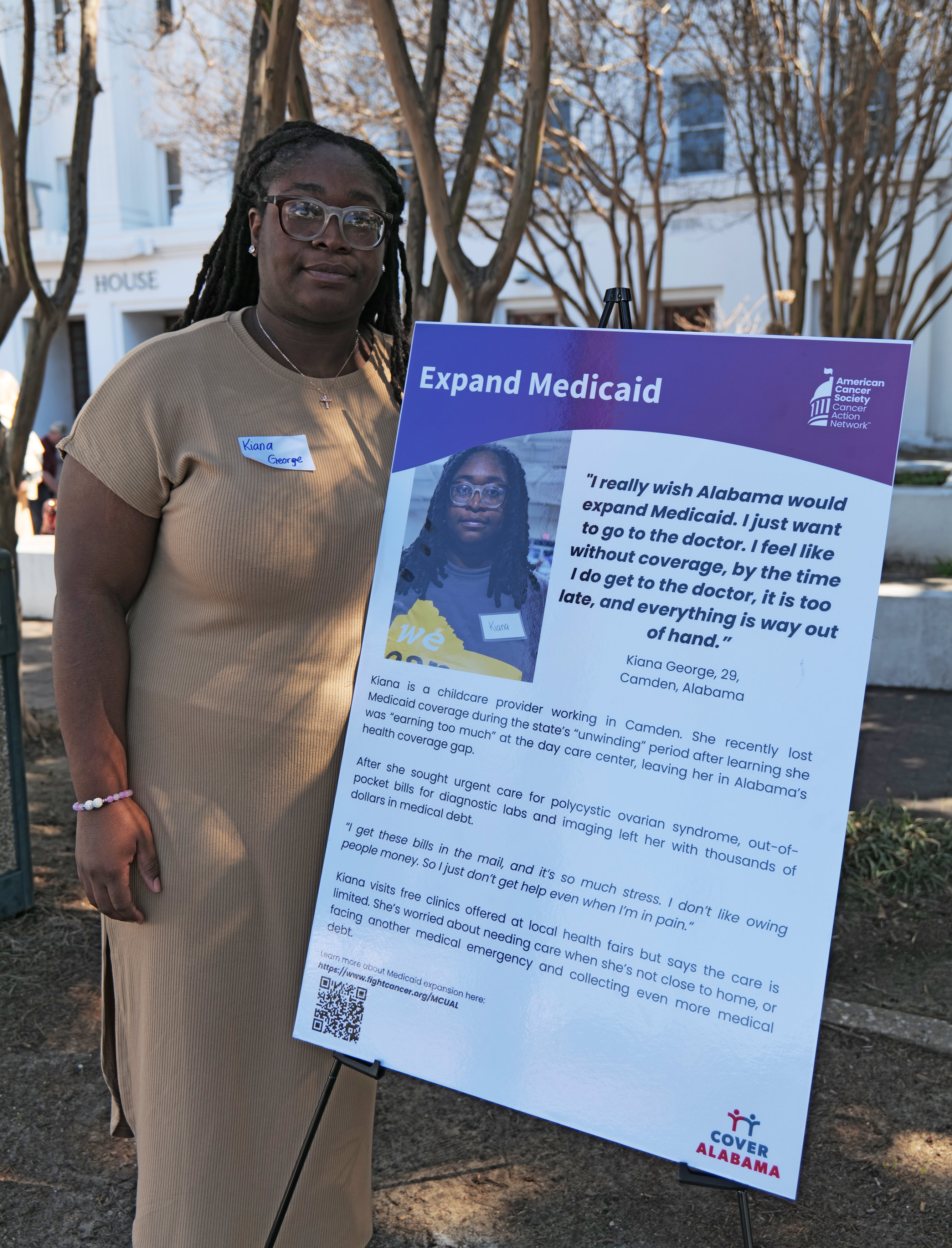

In January, Camden, Alabama, resident Kiana George, who’s uninsured, landed in an intensive care unit months after she stopped seeing a nurse practitioner and taking blood strain drugs — an ordeal that saddled her with practically $7,000 in medical payments.

George, 30, was kicked off Medicaid in 2023 after she acquired employed by an after-school program. It pays $800 a month, an earnings too excessive to qualify her for Medicaid in Alabama, which hasn’t expanded to cowl most low-income adults. She additionally doesn’t make sufficient for a free or reduced-cost ACA plan.

George, who has a 9-year-old daughter, mentioned she “has no concept” how she will repay the debt from the emergency room go to. And since she fears extra payments, she has given up on remedy for ovarian cysts.

“It hurts, however I’m simply gonna take my possibilities,” she mentioned.

Widening the Gaps

Medical health insurance is basically a monetary product, supposed to guard the policyholder’s pocketbook from accidents or sicknesses.

Researchers have identified for many years {that a} lack of insurance coverage protection results in poor entry to well being care, mentioned Tom Buchmueller, a well being economist on the College of Michigan Ross College of Enterprise.

“It’s solely extra just lately we’ve had actually good, robust proof that reveals that medical insurance actually does enhance well being outcomes,” Buchmueller mentioned.

Analysis launched this spring by the Nationwide Bureau of Financial Analysis discovered that increasing Medicaid decreased low-income adults’ possibilities of dying by 2.5%. In 2019, a separate examine printed by that nonpartisan suppose tank supplied experimental proof that medical insurance protection decreased mortality amongst middle-aged adults.

In late Might, the Home narrowly superior the finances laws that impartial authorities analysts mentioned would end in tens of millions of Individuals dropping medical insurance protection and scale back federal spending on applications like Medicaid by billions of {dollars}.

A key provision would require some Medicaid enrollees to work, volunteer, or full different qualifying actions for 80 hours a month, beginning on the finish of 2026. Most Medicaid enrollees already work or have some cause they will’t, corresponding to a incapacity, in keeping with KFF.

Home Speaker Mike Johnson has defended the requirement as “ethical.”

“If you’ll be able to work and also you refuse to take action, you might be defrauding the system. You’re dishonest the system,” he instructed CBS Information within the wake of the invoice’s passage.

A Senate model of the invoice additionally consists of work necessities and extra frequent eligibility checks for Medicaid recipients.

Fiscal conservatives argue an answer is required to curb well being care’s rising prices.

The U.S. spends about twice as a lot per capita on well being care as different rich nations, and that spending would develop underneath the GOP’s finances invoice, mentioned Michael Cannon, director of well being coverage research on the Cato Institute, a suppose tank that helps much less authorities spending on well being care.

However the invoice doesn’t handle the foundation causes of administrative complexity or unaffordable care, Cannon mentioned. To try this would entail, as an illustration, removing the tax break for employer-sponsored care, which he mentioned fuels extreme spending, raises costs, and ties medical insurance to employment. He mentioned the invoice ought to minimize federal funding for Medicaid, not simply restrict its development.

The invoice would throw extra folks right into a high-cost well being care panorama with little safety, mentioned Aaron Carroll, president and CEO of AcademyHealth, a nonpartisan well being coverage analysis nonprofit.

“There’s a ton of proof that reveals that for those who make folks pay extra for well being care, they get much less well being care,” he mentioned. “There’s a lot of proof that reveals that disproportionately impacts poor, sicker folks.”

Labon McKenzie, 45, lives in Georgia, the one state that requires some Medicaid enrollees to work or full different qualifying actions to acquire protection.

He hasn’t been in a position to work since he broke a number of bones after he fell via a skylight whereas on the job three years in the past. He acquired fired from a county highway and bridge crew after the accident and hasn’t been authorised for Social Safety or incapacity advantages.

“I can’t get up too lengthy,” he mentioned. “I can’t sit down too lengthy.”

In February, McKenzie began seeing double, however canceled an appointment with an ophthalmologist as a result of he couldn’t provide you with the $300 the physician needed upfront. His cousin gave him an eye fixed patch to tide him over, and, in desperation, he took expired eye drops his daughter gave him. “I needed to attempt one thing,” he mentioned.

McKenzie, who lives in rural Fort Gaines, needs to work once more. However with out advantages, he can’t get the care he must turn into effectively sufficient.

“I simply need my physique mounted,” he mentioned.

Have you ever just lately misplaced your medical insurance protection? Have you ever been uninsured for some time? Click on right here to contact KFF Well being Information and share your story.

{kind=link}